The United States is currently in the midst of the second longest expansion in the nation’s history at 111 months and counting. In July of next year, we will officially be in the midst of the longest expansion on record.

Will we make it? Odds are almost certain we will. Far from losing steam, the U.S. economy has been on a solid upswing lately.

But as always, a deeper look at the data suggests that there are issues to keep an eye on. All in all, we remain pessimistically optimistic. Or perhaps optimistically pessimistic.

A Deeper Look

Consider some recent statistics.

• U.S. gross domestic product (GDP) growth in the second quarter came in above 4%, the best reading since 2014 and driven by strong growth in business and consumer spending.

• Industrial production is up 4% from one year ago—another recent best.

• Employment growth over the last 3 months has totaled more than 200,000 jobs added per month, even with unemployment below 4%. More importantly, the job openings rate is at 4.2%, suggesting that employers would hire even more workers, if they could find them.

The recent GDP release came with (as is usual every couple of years) a revision of the last few years of data on the basis of better data and improved techniques. While the revision didn’t change much in terms of the estimation of economic output, it did change the estimated flow of income.

In particular, the Bureau of Economic Analysis increased its estimate of proprietor incomes (earnings for the self-employed) substantially. This had the impact of completely erasing the decline in consumer savings rates we have been fretting about in recent reports.

Combine this with the low rate of consumer debt increases, and it is clear the overall financial health of U.S. households is as good as it has ever been.

Temporary Surge

As positive as all this news is, don’t be fooled into believing the U.S. economy has truly achieved a new pace of growth. Scratch away at the surface and there are any number of reasons to conclude that the current growth surge is, at best, temporary. At worst, the seeds of the next recession are possibly being sown in these current numbers.

• First, we need to take a bit of a gut check on the recent numbers. The 4.1% growth rate in the second quarter was certainly impressive. But most of that growth came from a surge in consumer spending—an anticipated surge given the weak first quarter for consumer spending growth.

In other words, it was a reversion to the trend, not a permanent jump. Business spending was solid, but similar to the last few years. Housing remains weak, as does state and local spending. The consensus outlook suggests growth will come in at a far more reasonable 3% for the balance of the year, with an average growth rate of 3% for the entire year.

This 3% pace of growth is not bad relative to the 2% to 2.5% pace seen since the end of the Great Recession. But even here, it is important to recognize that this modest bump is being driven by a surge in government borrowing rather than any true shift in fundamentals.

The tax plan passed at the end of last year was not the major overhaul of a broken tax system that the United States desperately needs. Rather, it was nothing more than a fiscal stimulus plan, something that would typically be used in times of economic trouble—not in the midst of a record tight labor market.

The problem with any fiscal debt-driven stimulus is that you are borrowing from the future to accelerate the “now.” And like most stimulants, the buzz you get feels good in the short run, but diminishes over time unless you continue to increase the dosage. Then there is always the inevitable crash, when you finally have to get off of the stimulant completely. When that crash will occur for the economy is unclear, but the current path is guaranteeing that when that day comes, it will be ugly.

• Second are the international trade battles currently in play. While the problems with the European Union seem to be on hold for the moment, the U.S. disputes with China are growing worse with both sides continuing to ratchet up the tariffs being levered on the other. Much has been made of the effects on U.S. exporters to China, particularly those that export agricultural products. But the U.S. imports almost four times as much from China as it exports to them. And what we do import are critical components of U.S. supply chains. As solid as industrial production looks from a growth perspective, recent data suggests overall production is starting to plateau.

This is not to say that some of this isn’t good pain—the Chinese have been flouting international norms on trade, intellectual property rights, and foreign investment for years, and that needs to end. The U.S. does need to push back, but to do so, negotiations must start with a clear and logical set of goals. War for war’s sake is never a good plan.

Unfortunately, the current administration appears to have no clear path forward, and with other troubles brewing, including possible legal problems, it seems unlikely that it will be able to develop a coherent and effective plan any time soon. And let’s not forget that the North American Free Trade Agreement (NAFTA)—by far the most important trade group for the U.S.—also is under threat.

• Lastly, there is the Federal Reserve. Inflation has heated up as of late with the Consumer Price Index (CPI) getting close to 3%, the fastest since 2011. Beacon Economics, however, still doesn’t believe there is a real chance of higher permanent inflation. M2 growth remains below 4%, and bank lending is tepid.

But with employment costs and import prices on the uptick, the Fed will surely continue to tighten regardless of the impact on the yield curve. This too will place stress on the economy.

Add it up and the rest of this year looks solid, but expect slower growth next year. Additionally, the long-term stressors of heavy federal borrowing, rising interest rates, and ongoing political chaos, make it clear that while there is no reason to expect a recession anytime soon, we should remain more vigilant than ever in watching for the unanticipated shock.

The nation’s capacity to absorb a blow to its economy is substantially diminished and it won’t take much to end the current expansion.

State Forecast: OK for Now

With two quarters down and sights turning toward the last part of the year, it is apparent that the California economic engine continues to hum along, much like the nation as a whole. Job gains have been steady and the state’s leading industries have expanded despite ongoing concerns on the international trade front.

Still, good news notwithstanding, anxieties linger about California’s extremely tight housing market and the resulting affordability challenges it presents, and the long-term consequences of slow growth in the state’s labor force.

2018 Shaping Up to Be Good Year

California continues to land in record territory, with its unemployment rate at 4.2% for the fourth month in a row as of July 2018. At the same time, job growth so far this year has outpaced 2017 by a slim margin, with wage and salary jobs in July increasing by 2.0% or 332,700 jobs compared to one year earlier.

Of the 332,700 jobs added in July, Health Care and Leisure and Hospitality each contributed 58,000 positions, or more than one-third of the total, with Construction, Professional Scientific and Technical Services, and Transportation and Warehousing also reporting sizable gains among the private sector industries. This set of industries has consistently made the largest contributions to job gains in the state over the last several years.

The Government sector added to its ranks as well, increasing by 33,300 workers with roughly two-thirds of the increase occurring in Local Government and one-third in State Government (the Federal Government trimmed 2,500 jobs).

All but one of the state’s major industries experienced job gains in July, with only Mining and Logging seeing a loss of 300 jobs.

Steady Job Gains

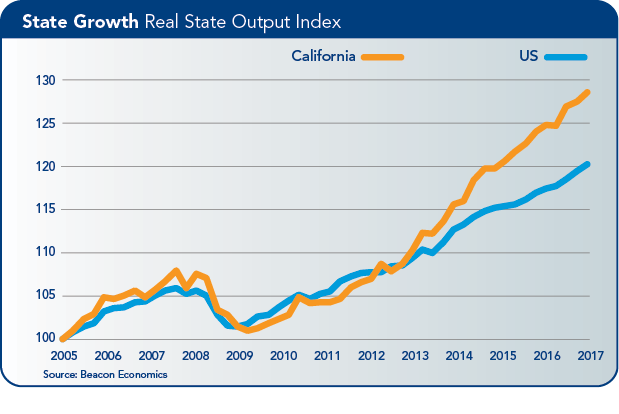

Similarly, headline numbers for California’s gross state product (GSP) and taxable receipts reveal continued growth in the statewide economy in the first part of the year.

Real GSP advanced by 3.5% year-to-year in the first quarter, the fastest rate of growth since late 2015, while current dollar taxable receipts grew by 4.3%.

A look at more detailed data shows healthy spending on the part of both households and businesses: Taxable receipts on consumer goods rose 4.8% year-to-year while receipts on business and industry spending increased by 3.6% over the same period.

Both the coastal and inland regions of the state have enjoyed economic and job gains for several years running. Through the first seven months of this year, every metro area in California experienced job growth. Across the large metro areas, job gains in the San Francisco Bay Area reflect the staying power of the tech sector, with the largest absolute and percentage increases occurring in San Jose.

In Southern California, the Inland Empire has consistently registered the largest percentage gains in jobs for the last couple of years, although Los Angeles County generally reports the largest absolute gains because of its size. Much of the growth in the entire region has come from Health Care, Professional Scientific and Technical Services, Construction, and Logistics. Metro areas in the Central Valley have also seen employment growth overall, supported by job gains across a variety of sectors.

Housing: Mixed Performance

California’s housing market has been a mixed bag so far this year. According to the California Association of Realtors, the monthly median home price in California finally surpassed its pre-recession peak earlier this year, a long-awaited milestone that signifies how far the market has come.

The median price in the state was $591,460 in July, up 7.6% year-to-year, continuing a string of yearly price gains going back several years. Still, home sales have been average, at best, and disappointing when considered against the backdrop of the state’s long economic expansion.

Home sales fell 0.9% year-to-year in July, and over the first seven months of the year were 1.4% lower in year-to-date terms. Sluggish sales are symptomatic of the state’s housing market, and due in part to tight lending standards on mortgages and lean supply (unsold inventory is still low at 3.3 months).

It is noteworthy, however, that the number of listings over the period spanning February through July was higher than in 2017, with listings in July 2018 alone up 15.2% from one year earlier. More listings should temper price increases going forward and slow the recent declines in affordability, which fell to a 10-year low in the second quarter of this year.

New home construction moved up a notch in the first half of this year compared with last year, a development that should also temper, but not halt, price increases. Overall, housing permits rose 9.4% in the first half of 2018 compared to one year earlier, with increases of 7.3% in single-family permits and 11.4% in multi-family permits.

The state is on track to add about 130,000 new units this year, still far below its needs, which are closer to 200,000 units annually. As long as home construction lags behind what the state needs, high housing costs will be a painful thorn in the side of the California economy.

Long-Run Concerns Linger

High housing costs impede California’s economic growth over the long term to the extent that these costs serve as a deterrent to labor force growth.

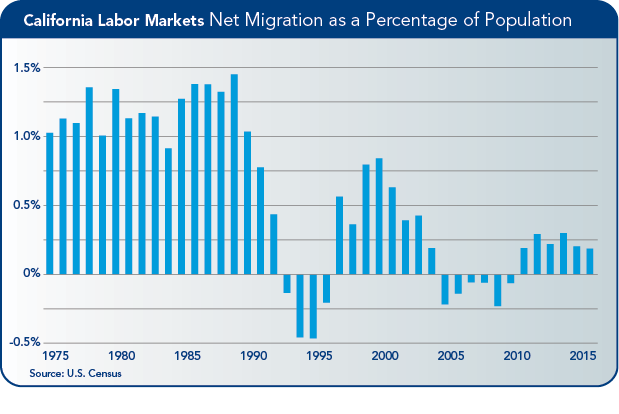

The state’s labor force growth rate has experienced significant slowing since the fall of 2017, with the year-to-year growth rate at just 0.2% in July 2018. Monthly labor force data are notoriously volatile, so a more consistent picture results from looking at 12-month moving averages of growth.

If anything, the longer-term story that emerges is more concerning. Over the last few years, the growth rate of California’s labor force followed roughly the same direction as the growth rate of the U.S. labor force—until the second half of 2017, when California’s growth rate began a steady decline even as the U.S. growth rate has accelerated in recent months.

In looking at the future growth trajectory of the California economy, the elephant in the room is the high cost of housing and its impact on labor force growth.

State-to-state migration data show an ongoing outmigration from California going back many years, which fortunately has been more than offset in most years by positive international migration into the state.

This is no accident: the California median home price has consistently been more than double the national median home price for several years. The rental market is no different, with a number of California metro areas ranking among the least affordable rental markets in the nation.

As growth in the state’s labor force slows further, it will tighten like a noose on the economy and limit future growth and business development.

The California Chamber of Commerce Economic Advisory Council, made up of leading economists from the private and public sectors, presents a report each quarter to the CalChamber Board of Directors. This report was prepared by council chair Christopher Thornberg, Ph.D., founding partner of Beacon Economics, LLC.

The California Chamber of Commerce Economic Advisory Council, made up of leading economists from the private and public sectors, presents a report each quarter to the CalChamber Board of Directors. This report was prepared by council chair Christopher Thornberg, Ph.D., founding partner of Beacon Economics, LLC.