The election that put Donald Trump in the White House in 2017 was a shock to the vast majority of pollsters who were predicting a win for Hillary Clinton. The outcome also is a shock to the staff at Beacon Economics whose economic outlook over the last year has implicitly been based on the (incorrectly) predicted outcome of a Clinton win. Our view assumed that her administration would largely continue current White House policies and that, combined with continued political gridlock in Washington, D.C., would reduce the chances of any major policy change.

The outcome of the election changes our outlook, albeit “how” is still an unknown. This will depend greatly on what happens in the first few months of the Trump administration. What we do know is that the potential upsides are limited, and the potential downsides are enormous—to the point that there is now a very real probability of a recession over the next two years.

U.S. Economy

Donald Trump’s victory clearly stems from the frustration, and ultimately the rejection of the status quo by many Americans. Trump fed this discontent with a steady stream of dystopian views about a U.S. economy in decline, driven by bad regulations, bad trade deals, and bad tax policies. But this was a triumph of rhetoric over reality, rather than the other way around, as many Trump supporters believe.

In reality, the United States still offers its citizens one of the best standards of living in the world, and continues to be in the midst of a steady, if mediocre, economic expansion. Yes, the U.S. economy has been growing at a below-average pace—particularly over the last few quarters when the economy was barely averaging 1% growth—but the nation also is in the midst of its seventh year of economic expansion. Given our current economic fundamentals, there had been little reason to think that would end anytime soon. Labor markets are at full employment, wages are starting to rise, and asset prices are at or near record high levels. And there was no October surprise—the initial read on gross domestic product (GDP) growth in the third quarter came in at a steady 3% after a weak first half of the year.

Consumer spending, despite a slower third quarter, remains one of the bright spots and sources of momentum in the U.S. economy. This may seem out of step with the rhetoric leading up to the election (Americans hurt by trade, families with no raise in 15 years, etc.), but this is because that rhetoric has been based on bad data, and even worse theories about the true state of the U.S. economy.

When properly and thoroughly accounting for sources of income, the data shows that Americans have seen solid gains in the standard of living over the last two decades, and we still remain at the top of the global consumption heap—consuming per capita 4 times more than the global average. There has been a modest slowing in job growth, but this is not due to a lack of demand for workers—the U.S. Bureau of Labor Statistics has estimated that the job openings rate remains at an all-time high level. Rather, the tight labor market is making it more difficult for employers to find the right employee.

The U.S. work participation rate has stopped falling—a very good sign since the aging of the nation’s workforce suggests it should continue to fall. People are being drawn back into the labor market in a significant way for the first time in a decade.

Business Investment

The recent drag in business investment stems largely from the commodity glut and the sharp declines in oil and natural gas exploration. Direct spending in the oil and gas industry dropped by more than $100 billion. The supply chain effects are long in this very capital-intensive industry, and once multiplier effects are included, the industry’s price collapse shaved almost a full percentage point off overall GDP growth in the last two years despite causing job growth to slow only imperceptibly.

And the oil and gas glut is still with us. Oil production in the United States is still greater than 8.5 million barrels per day, and there are record stocks of oil inventories, not to mention drilled, but uncompleted wells. Far from being dragged down by excessive regulations, the energy sector is largely a victim of its own success.

Residential Investment

The one surprising shift in the economy over the last few quarters is on the residential investment side—specifically as it relates to single family homes where spending has fallen since the peak in the fourth quarter of 2015, reducing the overall pace of GDP growth by a small amount over the year. This is the first time this has happened since the housing market collapse that began before the Great Recession.

But that is where any similarity between today’s housing market and the one that led up to the recession ends. This seeming contradiction can be traced back to mortgage credit problems that continue to negatively influence the housing recovery.

Prior to Dodd-Frank, families with credit scores below 720 still had opportunities to buy homes through a variety of higher interest rate mortgage products. Dodd-Frank sought to push the liability of a foreclosure from the borrower to the lender and the net result has been a sharp reduction in credit accessibility to these lower credit score households. This has held down the pace of new building, home ownership, and house sales—a problem that explains the overall softness of the market.

Despite these positive trends, throughout his campaign, Donald Trump has promised to enact numerous policies to “fix” the economy. And this is where the danger starts—as his populist agenda is full of dangerously simplistic ideas rather than sober assessments of feasible policy choices. Recessions are caused by real shocks to the economy that have three characteristics—they have to be large, rapid, and sustained. Here are three policy options voiced by Trump in his campaign that could create just such a situation.

Trump’s Proposals

• Slashing taxes will create a small modest positive impact on short-run growth, but only by blowing out the federal budget deficit and widening the trade deficit. These could lead to sharply rising interest rates and a devaluing dollar.

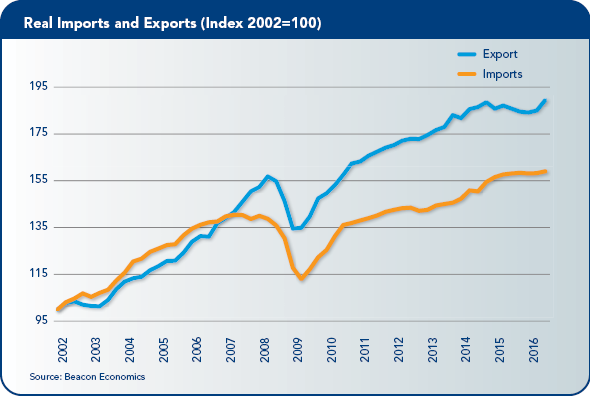

• If the United States under Donald Trump ends its commitment to free trade, backs out of the North American Free Trade Agreement (NAFTA) or the World Trade Organization (WTO), and starts a trade war with China, the result will be sharply falling imports AND exports, huge disruptions of supply chains, and a sharp rise in consumer prices.

• Trump also has threatened to find and deport millions of undocumented residents in the United States. Aside from the sheer scale of potential human tragedy here, this too would cause massive disruptions in supply chains and consumer spending.

Any of these three issues, if pursued vigorously, has the potential to cause a recession. This ignores the obvious long- term damage to the economy driven by his claims to unwind major policy advances in health care, environmental protections, education, and even basic economic data collection and the threat to put the Federal Reserve under congressional control.

In short, the election of Donald Trump represents a serious threat to the current health of the U.S. economy. How serious is unknown and depends on how well he gets along with Congress, how well Senate Democrats move to block changes in rules (expect the filibuster to be used a record number of times in coming months) and whether he appoints a cabinet with reasonable policy experts rather than firebrands.

What this means is that we just don’t know—and that is the scariest feeling of all.

California Outlook

California has stayed on course with a solid economic performance through the first three quarters of 2016 despite slower growth nationally. The state outdistanced the nation in terms of economic growth and job creation, although the pace of growth in both California and the United States has been somewhat slower than last year.

Virtually every industry in the state continues to add jobs and the unemployment rate is lower than a year ago. All in all, the statewide economy is poised for continued growth over the next several quarters, outpacing most other states in the nation.

California’s job market has been impressive over the last four years, with wage and salary (nonfarm) job growth that has exceeded the nation’s each year since 2012. In 2015, the state’s 3% growth rate placed it among the top 10 states in the nation. Through September of this year, nonfarm jobs grew at 2.6%, compared to 1.8% nationally. The state unemployment rate dropped below 6% late last year, moving sideways in the mid-5% range for much of the year as sustained job growth and wage gains have drawn more people into the labor force.

Virtually every industry in the state continues to add jobs in yearly terms. Health care and social assistance have led the way with the largest absolute job gains in the state. Significant contributions have also come from leisure and hospitality; professional, scientific and technical services; and construction, illustrating the breadth of job gains throughout the private sector of the economy.

Every private sector industry in the state added jobs with the exception of manufacturing, which lost 17,500 jobs on a base of 16.6 million.

Government also was among those industries seeing large absolute gains, with most of the increase occurring in state and local government.

Many of these same industries led the state in terms of percentage gains, although private education services outpaced all other sectors with a 6.7% year-to-year gain. Last, but not least, California’s farm employment is on track to hit its highest level in over a dozen years, despite the state’s prolonged drought.

Taxable Sales

In addition to steady job gains, spending activity statewide, as measured by taxable sales, has been growing steadily over the last few years. Following an increase of more than 4% last year, taxable sales were up by over 2% through the first half of 2016, with the busy holiday season still ahead.

Not unlike the nation, the consumer sector accounts for most of the spending activity in the state. Taxable receipts on consumer goods accounted for 60% of total taxable receipts last year, and saw a modest 1% gain in the first half of this year. Taxable receipts by businesses registered a 3.6% increase over the same period, providing further evidence of the strength of the state’s industries.

Regional economies across the state have grown over the last several quarters, with job gains that have varied from location to location. Over the past two years, economic growth has spread inland from coastal counties. Many parts of the state have hit new records for employment, and unemployment rates have declined to their lowest in several years.

Smaller regions may lead the state in terms of percentage job gains, but Los Angeles County routinely adds by far the largest absolute number of jobs from one month to the next, followed by the Inland Empire, Orange County, and San Diego County in the south. The Silicon Valley (San Jose-Santa Clara), San Francisco, and Sacramento routinely post the largest gains among metro areas in the northern part of the state.

Housing

The housing sector is important in its own right as a driver of the state economy, but it also serves as a gauge of the state’s economic health. The picture for housing has been mixed since the recession, with prices advancing modestly despite many hurdles that have limited sales activity.

Outside of the San Francisco Bay Area, home prices have yet to surpass their pre-recession peaks. Demand for homes has been sustained by continued low interest rates, but at the same time has been impeded by limited inventories, high underwriting standards, and large down payment requirements.

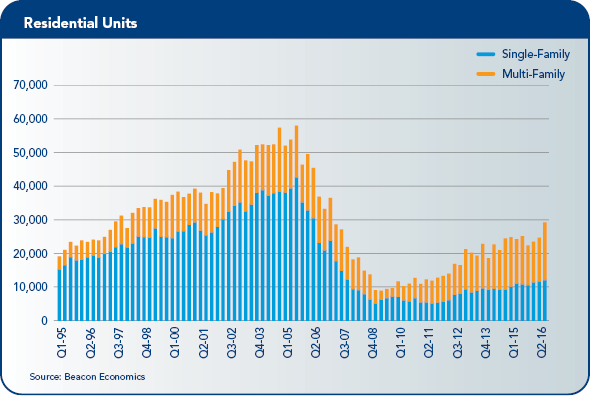

On the supply side, current homeowners have seen little reason to move and list their homes for sale, resulting in existing home supply that is well below long-run norms. Meanwhile, new home construction has struggled to advance since the recession, with permit levels that remain well below the long-run average, mainly because of a very slow rebound in single-family home construction. Through the first half of 2016 in California, total housing permits were 2% behind last year, with a 10.6% decline in multi-family activity nearly offset by a much-welcome 9% increase in single family activity.

If there is any part of the residential market that is bursting at the seams, it is the market for rentals. Throughout many metro areas of the state, high demand for apartments has driven vacancy rates down and rents up. Rents continue to head north despite a significant increase in multi-family construction over the last three years, the implication being that new supply has barely put a dent in the state’s chronic and long-standing shortage of units.

Demand for rentals has been strong in part because the market for owner-occupied homes has faced impediments (mentioned above). The homeownership rate was 53.2% in the third quarter of this year, the lowest in more than 30 years. This seems counterintuitive, given that the monthly payment for a typical home is well below its peak, owing to below-peak prices and historically low mortgage rates.

Would-be buyers in California, however, face significant hurdles in the form of high down payments and underwriting requirements that are very tight by historic standards.

On the nonresidential side of real estate, market conditions reflect the improvement seen across the sectors and regions of the statewide economy. For both office and retail, vacancy rates have edged down quarter by quarter in the metro areas of the state, while lease rates have risen.

Office lease rates in the San Francisco Bay Area, Los Angeles County, and Orange County have led the way in terms of increases. At the same time, industrial vacancy rates in Los Angeles County are among the lowest in the nation, having declined steadily in recent quarters, while lease rates have been climbing by low single-digit yearly percentages.

Looking out over the rest of 2016 and into 2017, the state’s economic engine will chug along. While growth may occur at a somewhat slower pace than in recent years, it should be noted that the U.S. economic expansion is approaching seven-and-a-half years in length, making it one of the longest on record. Businesses and households exercised greater caution in this expansion compared to previous cycles, but California’s economy has consistently outperformed all but a few states around the nation.

The technology sector continues to impress, not just in the Silicon Valley/San Francisco Bay Area, but also elsewhere in the state. Economic growth nationally will continue to drive the state’s tourism and goods movement industries, while health care and retail activity will see further gains as households across the state benefit from job growth and wage gains.

California continues to face nagging policy problems, not the least of which is housing. Rising home prices and rents mean that the state is not producing enough housing. This is not exclusively a low-income problem, but one that extends to middle-income households as well.

In many parts of the state, rent as a share of income exceeds the 30% threshold that is considered to be the norm. Meanwhile, in the market for owner-occupied homes, a household must earn at least $100,000 annually in order to afford the payment on a median-priced home in California. This has ramifications for employers who find it increasingly difficult to hire and retain qualified employees.

Solutions will be hard to come by, but must include reducing the permitting and regulatory burdens associated with construction costs, and possibly, tax reform.

Initiatives Assessment

This report assesses the results of three of California’s statewide ballot initiatives, each of which underscore the need for tax reform. And while a comprehensive reform of the state’s tax code is genuinely needed, spot reforms to parts of California’s tax structure could improve some fiscal outcomes.

• Proposition 51 passed, authorizing the state to borrow $9 billion in general obligation bonds for modernization and new construction of K-12 public school and community college facilities. This is just the latest school facilities bond measure, with voters approving a total of $102 billion in school facilities bonds since 1998, $36 billion at the state level, and $66 billion locally.

While few would argue against investing in public education facilities in particular, there is a broader concern about the extent to which California has encumbered itself with debt.

As of October 1, the state has $74.1 billion in outstanding general obligation long-term debt. Given the volatility of California’s finances in recent decades (see Proposition 55 discussion), servicing California’s debt obligations may come at the expense of other programs under normal circumstances and may be jeopardized when the state plunges into a budget crisis.

• Proposition 55 passed and extends by 12 years the tax increases passed in 2012 on California’s highest income earners. While the goal may have been to stabilize the state’s fiscal situation, passage of this measure may actually do the opposite.

California’s top-heavy income tax brackets already ensure that the state’s top 1% of taxpayers accounts for 40% or more of the state’s total income tax collections. Because the incomes of these taxpayers are quite volatile, however, the state’s revenue stream is subject to wide swings that tend to be pro-cyclical, wreaking havoc on government programs from K-12 education to prisons.

This pattern is well-known, with past budget crises occurring nearly every decade. Rather than stabilizing the state’s budget, this measure locks in volatility and ensures that the state will hurdle from one tax crisis to another. This underscores the need for comprehensive reform of state and local taxes, from income taxes to property taxes and beyond.

• Proposition 64’s passage legalizes marijuana for recreational use in California. The state is by no means the first to do so, but legalizing recreational use of marijuana will have many implications for residents. The measure is expected to reduce public safety and criminal justice costs by several million dollars annually, while creating a new source of tax revenues at the state and local level.

How big of a revenue source? It depends. Simply legalizing recreational marijuana may lead to increased consumption, but consumption will rise further as the price of marijuana falls in response to production and supply increases.

California may learn from Colorado’s experience: In 2015, state and local government collected $135 million in tax revenues on the sale of nearly $1 billion in marijuana, up from $700 million in 2014. Wholesale marijuana prices, however, have fallen by nearly half over the past year, so tax collections are likely to fall below expectations in 2016.

The California Chamber of Commerce Economic Advisory Council, made up of leading economists from the private and public sectors, presents a report each quarter to the CalChamber Board of Directors. The U.S. forecast in this report was prepared by council chair Christopher Thornberg, Ph.D., founding partner of Beacon Economics, LLC. The California forecast was prepared by Robert Kleinhenz, Ph.D., director of economic research at Beacon Economics.

The California Chamber of Commerce Economic Advisory Council, made up of leading economists from the private and public sectors, presents a report each quarter to the CalChamber Board of Directors. The U.S. forecast in this report was prepared by council chair Christopher Thornberg, Ph.D., founding partner of Beacon Economics, LLC. The California forecast was prepared by Robert Kleinhenz, Ph.D., director of economic research at Beacon Economics.