California employers can expect a higher federal unemployment insurance (UI) tax bill when it arrives this month.

This year will be the sixth in a row that California will have been in debt to the Federal Unemployment Trust Account (FUTA). Each year that a balance is owed to the FUTA, California employers pay a higher tax that goes to pay down the debt and the state must pay interest on the outstanding debt. By the end of 2015, the state will have paid almost $1.3 billion in interest to the federal trust fund.

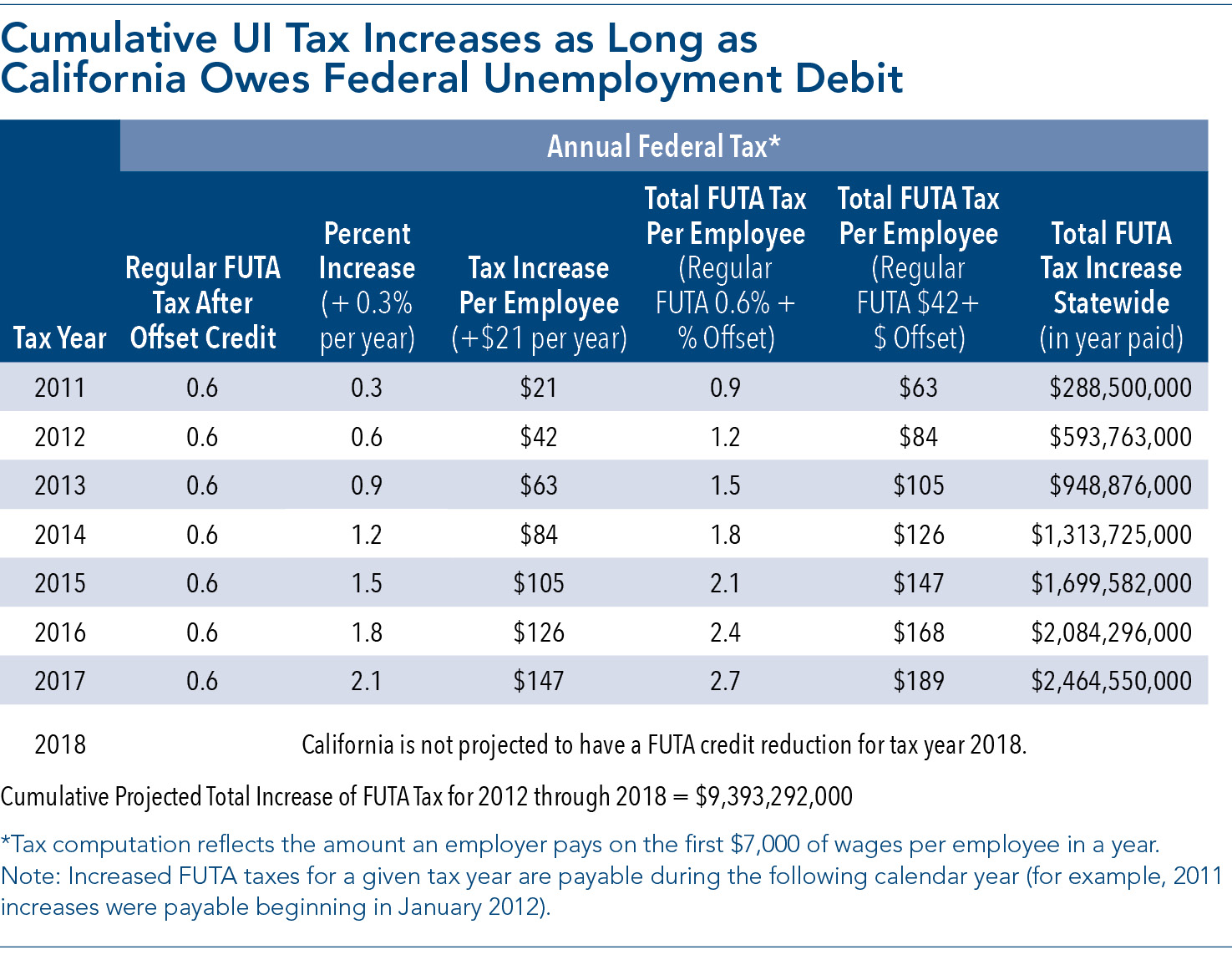

The federal tax on employers increases $21 per employee, per year until the debt is eliminated.

The federal UI tax to be paid by employers in California for 2014 was $126 per employee (1.8% on a $7,000 tax base, which includes an additional 1.2% on top of the normal 0.6%). The maximum tax for 2015 is $147 per employee, and in 2016 it is projected to be $168 per employee (see table).

FUTA taxes are due January 31 of the year following the year in which the taxes are applied. The federal UI tax is in addition to the state UI tax (maximum 6.2% on the first $7,000 of wages per employee), and goes directly to pay down the state’s debt to the fund.

Cumulative UI Tax Increases as Long as California Owes Federal Unemployment Debit

|

Tax Year |

Annual Federal Tax* |

|||||

|

Regular FUTA Tax After Offset Credit |

Percent Increase |

Tax Increase Per Employee (+$21 per year) |

Total FUTA Tax Per Employee (Regular |

Total FUTA Tax Per Employee (Regular |

Total FUTA Tax Increase Statewide |

|

|

2011 |

0.6 |

0.3 |

$21 |

0.9 |

$63 |

$288,500,000 |

|

2012 |

0.6 |

0.6 |

$42 |

1.2 |

$84 |

$593,763,000 |

|

2013 |

0.6 |

0.9 |

$63 |

1.5 |

$105 |

$948,876,000 |

|

2014 |

0.6 |

1.2 |

$84 |

1.8 |

$126 |

$1,313,725,000 |

|

2015 |

0.6 |

1.5 |

$105 |

2.1 |

$147 |

$1,699,582,000 |

|

2016 |

0.6 |

1.8 |

$126 |

2.4 |

$168 |

$2,084,296,000 |

|

2017 |

0.6 |

2.1 |

$147 |

2.7 |

$189 |

$2,464,550,000 |

|

2018 |

California is not projected to have a FUTA credit reduction for tax year 2018. |

|||||

Cumulative Projected Total Increase of FUTA Tax for 2012 through 2018 = $9,393,292,000

*Tax computation reflects the amount an employer pays on the first $7,000 of wages per employee in a year.

Note: Increased FUTA taxes for a given tax year are payable during the following calendar year (for example, 2011 increases were payable beginning in January 2012).

Funded by Taxes on Employers

California’s UI program is funded exclusively from taxes on employers, with the exception of temporary federal grants for administration and certain emergency and extended benefits paid by the federal government. The state of California administers its UI program through the Employment Development Department (EDD) within the guidelines established under federal and state law.

California employers pay annual taxes on the first $7,000 in wages paid to each employee. Each employer pays a tax rate based in part on the amount of benefits that have been paid to former employees so the tax is partly experience rated.

During good economic times, employers that have fewer claims generally are rewarded with a lower tax rate. Because the California UI Trust Fund has been facing financial difficulties for some time, all employers in California are paying taxes under the highest rate schedule allowable under state law, plus a 15% solvency surcharge, which makes the highest state UI tax rate 6.2%, plus the higher federal UI tax that goes to pay down the debt.

Reduced Federal Tax Offsets; Higher Taxes on Employers

Generally, employers receive a credit against the FUTA tax rate. Due to California’s outstanding debt, however, California employers are subject to a credit reduction that results in an employer-paid federal tax increase on wages paid.

The federal statute requires the federal government to incrementally reduce the offset credits to employers in states that do not timely repay their federal unemployment trust fund loans.

A federal tax normally is due on wages paid by employers at a rate of 6%, offset by a credit of 5.4%, for a payable rate of 0.6% on wages up to $7,000 a year.

Since January 1, 2011, California employers have been paying higher taxes because the state has not repaid money it borrowed from the federal government to pay UI benefits since 2009. The higher tax will remain in effect through 2016 and continue to increase each year the state has an outstanding loan balance.

Insolvency Factor

California’s current UI fund insolvency is caused not only by significant unemployment, but also can be traced back to the UI benefit increases imposed in 2001. The California Chamber of Commerce opposed this increase in benefits because it was not coupled with cost savings. Further exacerbating the situation, as unemployment and duration of benefits increased, the state collected fewer tax revenues and paid more benefits to unemployed Californians.

With the annual UI benefit obligation projected to be around $5.7 billion in 2015 and $5.6 billion in 2016 and 2017, California can expect its UI Trust Fund to be in debt about $2 billion to the federal trust fund by the end of 2017, down from a high of $10.2 billion at the end of 2012.

If California’s economy continues to improve as anticipated while generating sufficient UI tax receipts to pay ongoing benefits, the principal debt will be paid off in 2018 and the FUTA offset credit will be fully restored to employers.

Congressional Activity

While various proposals were floated in 2015, little concrete action was taken by Congress or the President to address UI solvency, taxes or benefits. Legislation backed by the professional employer organizations (PEOs) was enacted and effective January 1, 2016, recognizes PEOs as employers for federal unemployment tax reporting purposes.

President Barack Obama’s budget proposed an increase in the FUTA wage base but was not considered by Congress. Given the improving economy nationwide, most states have resolved their UI fund issues by paying off their federal loans from the FUTA and implementing a variety of reforms, including decreasing benefit payout, relieving the urgency for federal action to resolve state debt issues.

More Information

EDD has advised employers with questions on the FUTA credit reduction, Form 940 or Publication 15 (2011) (Circular E) Employer’s Tax Guide to contact the IRS at www.irs.gov.

{kind=link}